Tax-Sensitive Investment Planning In 2023

2023 is shaping up as an action-packed year for tax and financial planning maneuvers. With a 19.6% return on the Standard & Poor’s 500 stock in the first six months of 2023 and a much faster than expected 2.4% gross domestic product growth rate in the U.S. economy, stock prices and the economy have risen much more than expected.

The surprising gains on capital-gains producing assets, like stocks and housing, make this a good time to consider converting assets in traditional IRAs and taxable accounts to Roth IRAs. Conversions of investments in traditional IRA accounts to Roth IRA accounts involve selling investments that rose sharply in the first half of 2023 and will likely require paying income taxes on the sale proceeds.

However, if you believe Federal taxes are likely to rise in the next decade to finance the long-term U.S. debt, it’s wise to consider moving assets into Roth IRA accounts by the end of 2023 because Roth IRAs are not subject to income tax annually or upon withdrawal.

The U.S. long-term debt is expected to grow significantly in the next decade to pay for annual deficits and rising interest payments to fund Social Security and Medicare. Without government action, paying only the interest on the debt becomes unsustainable in about a decade and mushrooms out of control, according to the Congressional Budget Office (CBO), a non-partisan arm of the U. S. Congress. With U.S. tax rates compared to Germany, France, and other developed nations relatively low, a tax increase in the U.S. is likely.

A tax increase would make tax-free investments more valuable to a retiree. Converting taxable investments to Roth IRAs, which grow tax-free and generally are not taxed upon withdrawal in retirement, may make a lot of sense in 2023.

Selling profitable taxable capital investments before the end of 2023, and writing off any capital losses sustained this year, would free up funds for a Roth IRA account that generates tax-free income when you’re retired. This type of tax-sensitive investing is a way of boosting after-tax returns by strategically planning the location of your investments, so they’re held in accounts with the goal of optimizing after-tax income in retirement.

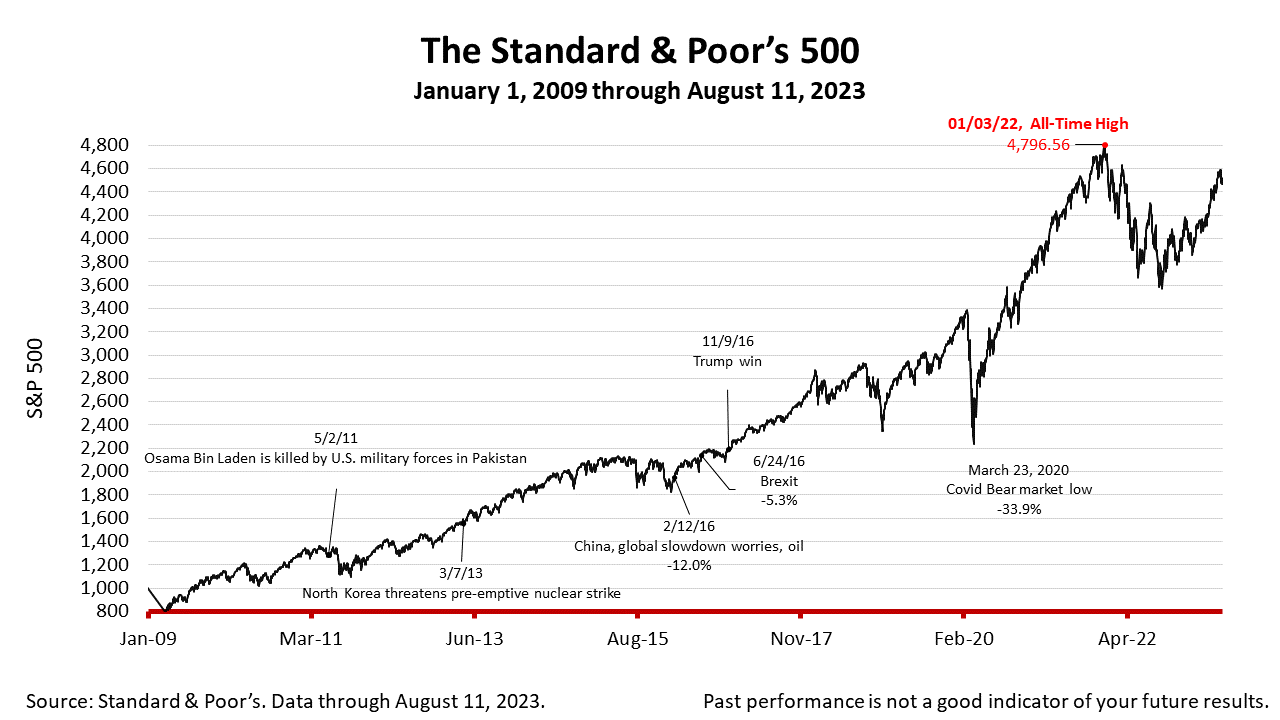

The Standard & Poor’s 500 stock index closed Friday at 4464.05, down -0.11% from Thursday, and -0.31% from a week ago. The stock index is up 99.52% from the March 23, 2020, bear market low and only -6.93% lower than its January 3, 2022, all-time high.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market-value weighted index with each stock’s weight proportionate to its market value. Index returns do not include fees or expenses. Investing involves risk, including the loss of principal, and past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Financial Services for Real People

Founded for the benefit of clients, Prism Capital Management is an independent Seattle and Skagit-based firm with a deep commitment to providing guidance that is free of conflicts of interest, based solely on the sum of our experience and expertise. We are committed to putting client interests first and to stewarding both wealth and well-being for those we serve. We have a singular measure of success: the results we get for our clients.

As an Investment Advisor, we have a fiduciary duty to act in YOUR best interest. From planning to investment management to advice on buying a car, we are your financial life partners.

Schedule a FREE Consultation Today!